Change is one of those things that we all know is necessary but often struggle with. Whether it’s a change in our spending habits, our health routines, or our approach to relationships, the process can be daunting. The desire to improve is there, but the path forward isn’t always clear or easy. This is where the concept of “nudging, not judging” can be transformative.

It’s about guiding ourselves and others toward positive change with gentle encouragement rather than harsh criticism. When it comes to financial planning, this philosophy is particularly powerful. Let’s be honest—money is a sensitive subject!

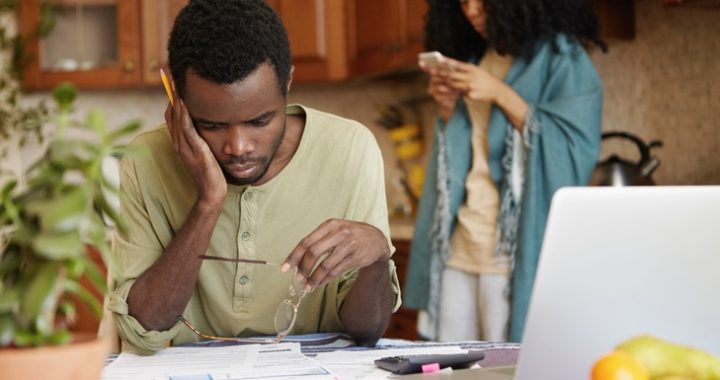

We often feel judged, not just by others, but by ourselves, when we don’t make the “right” decisions. We look at our past financial mistakes and wonder why we didn’t do better. But this self-judgment only deepens the sense of failure and can keep us stuck in a cycle of guilt and avoidance.

Instead, what if we approached financial change with a “nudge-ment” rather than a judgment? A nudge is a small, positive reinforcement or a gentle prompt that encourages us to make better decisions. It’s not about drastically overhauling our entire financial life overnight. It’s about making incremental improvements that, over time, lead to significant progress.

For example, let’s say you want to start saving more but haven’t been able to make it happen. Instead of judging yourself for not saving enough, start by setting up a small automatic transfer from your checking account to your savings account each month. This simple nudge helps build the habit of saving without the pressure of making a huge financial sacrifice all at once. Over time, as your savings grow, you might find it easier to increase that amount—because the habit is already in place.

Nudging can also be applied to how we interact with others about money. Too often, conversations about finances can become tense or judgmental, particularly in relationships or families. By adopting a nudge approach, we can foster a more supportive environment for discussing money. Instead of criticising a partner for their spending habits, for instance, we might suggest a joint goal that requires both of you to save a little more each month. This way, you’re working together toward a positive outcome rather than focusing on past mistakes.

The power of nudging lies in its subtlety. It recognises that change is a process, not an event. Small, consistent actions, driven by encouragement rather than criticism, create a foundation for lasting change. And the best part? These small changes often lead to a ripple effect, where one positive action leads to another, creating momentum that makes larger changes feel more achievable.

So, as you think about the changes you want to make in your financial life, remember the power of the nudge. Start with one small step, encourage yourself along the way, and let go of the harsh judgments that hold you back. Because in the end, it’s the consistent, positive nudges that lead to the most meaningful and sustainable change.